The Ongoing Recession and Its Ripple Effects on the IT Sector

Executive Summary

This report examines how the ongoing global slowdown is reshaping tech strategy for mid-sized firms—particularly in the U.S. and Europe. With IT budgets under pressure and internal hiring increasingly difficult to justify, companies are reassessing how and where they source critical technology talent.

India continues to offer a compelling mix of scale, technical depth, and rising AI adoption. The real opportunity lies in mid-tier partners who balance cost-efficiency with structured delivery and contextual thinking—offering the flexibility needed in today’s cycle, without compromising long-term scalability.

This piece outlines why the right global partnerships—and not just the cheapest ones—may be key to building resilient, capital-efficient tech teams in a post-AI world.

The Macroeconomic Backdrop: A Catalyst for Tech Recalibration

The signs have been building for months—and they’re becoming harder to ignore. Economic uncertainty appears to be tightening its grip on the US, with everything from trade policy to corporate earnings pointing to a possible slowdown. Goldman Sachs recently raised the probability of a U.S. recession to 45% (Source: Reuter, Apr 2025), and J.P. Morgan has flagged global risks that suggest this may not just be a passing blip (Source: JPMorgan Insights, Mar 2025).

At the centre of this uncertainty is a broader hesitance—one likely shaped by elevated interest rates, cautious consumer spending, and political volatility, especially with the possibility of a second Trump term. As a result, many businesses seem to be rethinking everything from capital allocation to hiring.

The US IT sector—previously viewed as a reliable engine of growth—is now showing signs of stress. Over 88,000 tech professionals have been laid off in just the first quarter of 2025 (Source: TechCrunch, Apr 2025). Google has reportedly trimmed roles across its Android and Chrome teams (Source: New York Post, Apr 2025), while Meta’s most recent restructuring affected nearly 4,000 employees globally (Source: Business Insider, Feb 2025). The broader trend suggests that budgets are being reviewed, timelines stretched, and hiring put on pause.

New tariffs—some reportedly as high as 104% on Chinese imports (Source: Investor’s Business Daily, Apr 2025)—could further exacerbate this by driving up costs and weakening demand in sectors like electronics and hardware. In this context, companies are beginning to reassess not just their financials, but also the structure and scalability of their operations.

Mid-sized companies, in particular, may be facing sharper constraints. Without the financial cushions larger firms rely on, these businesses could find it difficult to justify high fixed costs—especially when it comes to in-house IT talent that can easily cross the $200,000 mark per head. In such cases, looking outward for support may not just be a cost-saving measure, but a way to maintain operational flexibility in unpredictable times.

The Shift: Why Companies Are Looking Beyond Borders for IT Support

Economic slowdowns often prompt companies to reassess their operational strategies, particularly concerning high-cost functions like IT. As noted in our earlier section, the US tech sector is already seeing widespread budget tightening and a pullback in headcount—signalling the start of a larger recalibration.While some firms are reducing internal capacity, others are taking a different approach: rebalancing cost without losing technical momentum.

In Europe, the signals are different but no less important. The eurozone area is projected to grow at a modest 1.3% in 2025 (Source: EY), suggesting a cautious economic recovery. Though not in full recession, companies across the continent appear to be adopting a defensive posture, revisiting discretionary spends and looking for operational efficiency wherever possible.

In this context, developing countries have emerged as viable partners for IT support. Nations like India, Vietnam, and the Philippines offer a combination of skilled talent, cost advantages, and growing technological infrastructure. In fact, Europe’s IT outsourcing market is projected to reach $193.05 billion by 2025, up significantly from pre-pandemic levels (Source: statista.com).

This trend points to a clear recalibration—not just among large enterprises, but also among mid-sized firms seeking agility without burning through capital.

Europe’s Economic Outlook and IT Needs

While the eurozone area is expected to avoid a deep recession, growth is expected to remain subdued, with GDP expanding by just 1.3% in 2025 (Source:Europe’s Economic Outlook for 2025, EY). This slow recovery, coupled with ongoing fiscal constraints and inflationary pressures, appears to be prompting companies to stretch their tech budgets further.

Across broader Europe, including non-eurozone economies like the UK and Switzerland, similar themes are emerging—cautious spending, selective hiring, and an increased interest in outsourcing high-skill functions to trusted external partners.

As a result, European companies—both within and outside the euro area—are steadily leaning on IT providers in cost-competitive markets, particularly for cloud migration, automation, and cybersecurity support (Source: ECB, 2025)

India: The Global Backbone of IT

While global headlines often focus on big tech layoffs, funding winters, or the next AI breakthrough, India has quietly remained the global backbone of IT—powering systems, teams, and transformations across the world.

For decades, Indian IT service providers have supported some of the most complex and mission-critical systems globally—from core banking infrastructure and enterprise automation to product development and cybersecurity. According to NASSCOM, India remains the top preferred location for outsourcing digital services, with 53% of global enterprises choosing India among their top three destinations (Source: NASSCOM press release, Feb 2024). The country’s technology industry crossed $253.9 billion in revenue in FY24, growing at 3.8% year-on-year (Source: Business Standard, Feb 2024).

What’s changed in recent years is not just the scale—it’s the strategic depth. Indian firms are no longer seen as transactional vendors, but as long-term technology partners. They’re embedded in product teams, co-owning outcomes, and offering consultative value far beyond traditional outsourcing.

Several structural factors continue to work in India’s favour:

• A large, English-speaking tech workforce (5M+ professionals, many trained in global delivery models);

• A robust STEM education ecosystem;

• And a tech culture that has rapidly matured to adopt agile, devops, and product-first approaches.

But where India stands out most in the current macro environment is its ability to offer this capability at a cost structure that’s fundamentally more sustainable. In recessionary times—when US and European companies are under pressure to do more with less—India offers a rare combination of technical quality, delivery consistency, and economic efficiency.

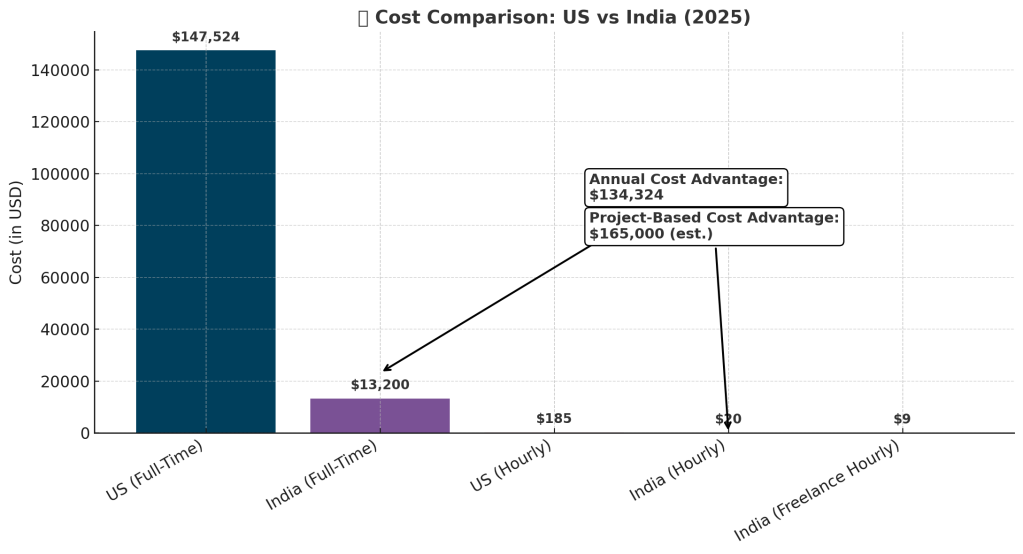

Salary Comparison: US vs India (Full-Time Engineers)

• United States: The average software engineer earns $147,524 annually (Source: ZipRecruiter)

• India: The average software engineer earns ₹11,00,000 (~$13,200 USD) annually (Source: PolarisCampus)

Of course, not every company has full-time tech requirements. Especially during recessionary cycles, some firms—particularly mid-sized ones—may prefer to staff on a project basis or engage only when specific needs arise. This is where the hourly cost advantage becomes even more relevant.

Ad-Hoc Outsourcing Rates: Project-Based or Hourly

• United States: Hourly development rates typically range from $120 to $250 depending on seniority and firm size (Source: FullStack Labs)

• India: Project-based hourly rates range from $15 to $25 for comparable roles (Source: Clarion Technologies)

• SumatoSoft, which tracks global outsourcing trends, reports even lower rates in some cases, with Indian freelance/contract devs billing as low as $6 to $12 per hour, especially for smaller ad-hoc projects Technologies) (Source: SumatoSoft)

This stark contrast highlights the significant cost savings companies can achieve by partnering with Indian IT professionals, without compromising on quality.

Whether it’s maintaining legacy infrastructure for Fortune 500s or building new cloud-native platforms for startups, Indian teams have consistently demonstrated both technical depth and resilience under pressure. That’s precisely what developed-market companies need right now: partners who can scale, deliver, and adapt—without inflating fixed costs.

Why India’s Cost Advantage Works Best in the Mid-Tier?

While India’s developer ecosystem offers a clear cost advantage, pricing can vary significantly—and not always in ways that reflect true capability.

It’s tempting to anchor decisions on the lowest hourly rate. But ultra-low-cost developers (typically quoting under $15/hour) often operate without robust infrastructure or standardized delivery processes. Communication gaps, delayed iterations, and short-term execution mindsets are common pitfalls at this tier.

The most effective partners often sit in the $45–85/hour range—a tier where firms balance affordability with process maturity, cross-functional collaboration, and long-term alignment. Thesemteams tend to offer:

• Clear documentation and consistent communication

• Agile delivery methods with versioning and QA baked in

• Familiarity with Western product expectations and tooling

• Stable pods that minimize onboarding drag

• A bias toward building context—not just closing tickets

For mid-sized companies especially, this middle ground offers the best of both worlds: a materially lower cost base compared to onshore teams, without the risks that come from over-optimizing on price alone.

Why This Especially Matters for Mid-Sized Companies

IT outsourcing has long been associated with large corporations managing multi-country delivery models. But in the current macro environment, it’s the mid-sized segment that may have the most to gain—and perhaps the most to lose if they delay recalibration.

Mid-sized firms typically operate with leaner structures and narrower financial cushions. In periods of prolonged slowdown—like what we’re seeing now in the US and potentially Europe—cost structures that worked in a growth environment can begin to feel disproportionately heavy. Technology, while critical to day-to-day functioning, often becomes a high fixed cost with limited near-term elasticity.

For companies where full-time engineers command upwards of $150K per year, this becomes a difficult trade-off: maintaining technical continuity vs. protecting runway.

That’s where external partnerships—particularly with countries like India—begin to make more sense. This isn’t about replacing internal teams overnight. Rather, it’s about creating a cost-flexible operating layer that can be scaled up or down depending on demand cycles.

In practice, this could mean:

• Retaining core decision-makers in-house, while outsourcing execution-heavy tech work to lower-cost markets.

• Structuring ad-hoc builds, integrations, or sprints with external partners instead of hiring permanent headcount.

• Replacing hard-to-fill roles with outcome-based contracts from geographies where talent is both available and cost-efficient.

The idea here isn’t new, but what’s changed is how essential it might become for survival. Mid-sized firms that proactively diversify their tech delivery base could end up far more resilient than those tied entirely to high-cost internal teams—especially if economic softness persists longer than anticipated.

India, in particular, has a track record of delivering at scale for companies across sizes and sectors. And while the historical narrative has focused on cost arbitrage, the more relevant framing today is operational resilience: maintaining delivery, managing volatility, and extending your capital runway without stalling product roadmaps.

What About AI?

With AI accelerating at breakneck speed, a natural question is: why continue investing in talent—offshore or otherwise—if AI could just write the code?

It’s a valid concern, but one where the current data points to a more nuanced reality. AI is not replacing developers—it’s making the best ones significantly more productive.

McKinsey’s June 2023 report on generative AI refers to it as a “productivity amplifier”—one that creates the most value when paired with domain expertise, structured workflows, and human oversight. Tools like GitHub Copilot have been shown to reduce coding time by over 50% (Source: GitHub Research Blog, May 2024), but only when used by engineers who already understand the architecture and business context (Source: MIT, Nov 2024).

In practice, this means that every hire you make becomes more valuable, not less. The better your developers understand how to use AI in their workflow—whether it’s for code generation, debugging, or documentation—the more leverage they create across the product lifecycle.

But this isn’t just about individual productivity. AI-assisted development still relies heavily on:

• Human judgment for prioritization, sequencing, and product impact

• Cross-functional communication across product, design, and ops

• Structured delivery that can adapt to changing business logic

And on a macro level, India’s developer ecosystem is already embracing AI adoption faster than many global peers—with upskilling platforms, developer conferences, and engineering programs explicitly focused on Copilot, LLM integration, and AI-powered tooling. This positions India not only as a cost-efficient destination, but as one that’s leaning in early to the next wave of productivity enhancement (Source: NASSCOM).

So no—the rise of AI doesn’t eliminate the need for engineering talent. If anything, it makes the right teams more powerful. And the market is already rewarding firms that understand that distinction.

Last updated: August 2025

Subscribe for Research-Driven Perspectives

Get deep dives, startup analysis, and market insights by Shraddha Deshmukh — straight to your inbox.

Subscribe Now